Hotel Credit Card Authorization Process: How It Works, Step by Step

TLDR;

- Hotel credit card authorization runs across four stages: reservation, pre-authorization, check-in authorization, and check-out settlement. Each stage holds or charges a different amount

- Pre-authorization at check-in holds the room rate plus an incidental amount (typically $50 to $200 per night), reducing the cardholder's available credit for the duration of the stay

- AVS (address verification) and CVV checks run on the credit card authorization form when the hotel processes it as card-not-present

- Hotel authorization holds can take 7 to 30 days to release after checkout, longer than any other merchant category, because the final settlement amount differs from the pre-authorized amount

- The most common failure point in corporate hotel CC authorization is the form itself: it gets lost, filed incorrectly, or used for charges outside its stated scope. Virtual cards eliminate the form entirely

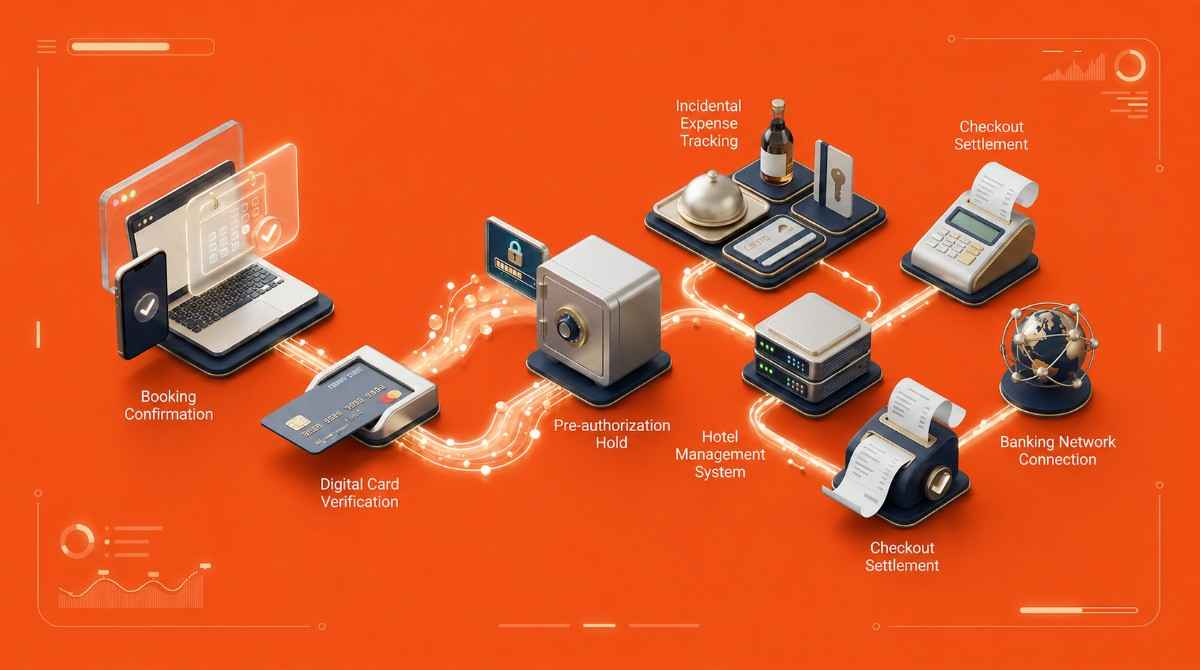

Hotel credit card authorization is the multi-stage process that holds and eventually charges a guest's card across the booking, the stay, and checkout. It is the area of payment authorization where corporate travel programs encounter the most disputes, because the hold amounts are larger, the windows are longer, and the payment process involves a credit card authorization form that traditional retail transactions don't use. This guide breaks down the four stages of hotel CC authorization end to end, what verification happens at each stage, how pre-authorization holds work, and why hotel holds release on a different timeline than every other merchant category.

What hotel credit card authorization actually is

Hotel credit card authorization is the verification and hold process that happens when a guest's card is used to secure and pay for a stay. It is not a single transaction. It is a sequence of authorizations and holds across the booking, the pre-arrival period, the check-in event, the duration of the stay, and the final checkout.

The reason hotels use a multi-stage process rather than a single charge at checkout is that the final amount of a hotel stay is rarely known at booking. Room rates can change with upgrades, incidentals (minibar, parking, restaurant) add up during the stay, and the final folio is only finalized at checkout. Hotels solve this by pre-authorizing an estimated amount up front and capturing the actual amount at the end.

Corporate travel adds a third layer to this: a credit card authorization form (CCA form) that lets the company pay for an employee's stay without the cardholder being physically present at check-in. The form is the friction point where most corporate hotel authorization problems start.

The 5 parties in a hotel credit card authorization

Every hotel credit card authorization involves the same five parties as a retail transaction, plus a paper or digital authorization form when corporate travel is involved.

- Guest (cardholder): The traveler or company representative whose card is being used.

- Hotel (merchant): The property accepting payment. Operates the property management system (PMS, such as Opera, Sabre SynXis, or Cloudbeds) that initiates the authorization request.

- Acquiring bank: The hotel's bank or payment processor. Routes the authorization to the card network.

- Card network: Visa, Mastercard, American Express, or Discover. Routes the request to the correct issuing bank based on the card's Bank Identification Number.

- Issuing bank: The cardholder's bank. Approves or declines based on funds, fraud signals, and verification checks.

When the corporate card is sent ahead via a CCA form, the form acts as a sixth element in the chain: the document that authorizes the hotel to charge a card the cardholder is not present to swipe.

The 4 stages of hotel CC authorization

Hotel CC authorization happens in four stages between the moment a guest books and the moment the final charge posts. Each stage holds or releases a different amount.

Stage 1: Reservation and booking

When the booking is made, the hotel may capture the card details and pre-authorize a small amount (typically $1 or the first night's room rate) to confirm the card is valid. For corporate bookings through a TMC or online booking tool, the booking system passes the corporate card details to the hotel as card-not-present payment, often via a credit card authorization form attached to the reservation.

This stage doesn't produce a hold large enough to affect the cardholder's available credit meaningfully. The hold typically clears within 1 to 3 business days if it doesn't roll into the check-in pre-authorization.

Stage 2: Pre-authorization at check-in

This is the largest hold of the stay. At check-in, the property pre-authorizes the card for the room rate plus an incidental amount, typically $50 to $200 per night for incidentals (minibar, restaurant, parking, damages). For a 5-night stay at $200 per night with $100/night incidentals, the pre-authorization is $1,500.

The pre-authorization is a hold, not a charge. The funds are reserved on the cardholder's available credit but don't post to the statement. The hold reduces available credit for the duration of the stay.

Two things happen at this stage that account for many hotel CC auth failures. AVS verification runs on the billing address the cardholder provided (especially relevant when a CCA form is in use because the address on the form must match the issuing bank's records). CVV verification runs if the card is being processed card-not-present.

Stage 3: During the stay

If incidental charges exceed the pre-authorized amount, the hotel may add incremental authorization holds during the stay. A $100/night incidental hold can grow to $300 if the guest spends $250 at the restaurant on night three. Each incremental hold runs the same verification path as the original pre-authorization.

Most properties consolidate these incremental holds rather than placing many small ones. Some properties place a daily incremental as a matter of routine. The result for the cardholder is that available credit can fluctuate during the stay even before the final settlement.

Stage 4: Checkout and final settlement

At checkout, the hotel calculates the actual folio (room nights, taxes, incidentals, any disputed charges) and submits the final amount for settlement. This is the only stage where money actually moves. Funds transfer from the issuing bank to the hotel's acquirer 1 to 3 business days later.

The pre-authorization hold from check-in does not automatically convert to the settlement. The hold and the settlement are separate transactions, which is why hotel holds can persist after checkout (more on this below).

How long does hotel credit card authorization take?

The authorization request itself completes in 1 to 3 seconds at each stage, just like any retail authorization. The total visible delay at check-in is usually 5 to 15 seconds because the property management system also reads the card, runs AVS and CVV checks, applies any fraud rules, and prints the registration card.

The release timeline is where hotels differ from every other category. After checkout, the pre-authorization hold and any incremental holds typically take 7 to 30 days to release. The variation depends on the card network (Visa typically releases faster than Amex on hotel categories), the hotel's processor, and whether the final folio amount matched the pre-authorization (matches release faster than mismatches).

The 30-day ceiling is the reason guests sometimes see "pending" charges on their statement for weeks after a stay. The funds aren't being charged; they're held against a settlement that has already happened separately. The cardholder's available credit eventually returns when the hold expires.

AVS, CVV, and the credit card authorization form

The verification checks that run during hotel pre-authorization deserve their own section because they account for most check-in declines on corporate cards.

- AVS (Address Verification Service): When the hotel processes a corporate card from a CCA form, the transaction is treated as card-not-present. AVS compares the billing address on the form against the address the issuing bank has on file. A mismatch produces a decline at most processors. Many CCA form declines that look like fraud blocks are actually AVS failures because the billing address on the form differs from the corporate card's registered address.

- CVV: The 3-digit (Visa, Mastercard, Discover) or 4-digit (Amex) security code on the card. CVV must be included on the CCA form for the property to authorize the card without it being physically present. A missing or incorrect CVV produces a hard decline.

- Form completeness: Beyond AVS and CVV, the form itself must include the cardholder name, card number, expiration, billing address, and an authorization signature. Missing fields cause the property to either decline the authorization or request the form be resent, which delays the booking.

Pre-authorization holds: amounts, lifecycle, and release

Hotel pre-authorization holds are larger and longer than any other merchant category. Understanding the lifecycle prevents the most common cardholder confusion.

- Amount: The pre-authorization at check-in is the full room rate for the stay plus the property's incidental policy. A 3-night stay at $250 per night with $150/night incidentals produces a $1,200 hold. Many luxury properties hold more aggressively (sometimes $500 per night incidentals), so the hold can reach four figures even on a moderate stay.

- Lifecycle: The hold persists from check-in until either settlement converts it to a charge or the hold window expires. Settlement typically happens at checkout (the property captures the final folio). The pre-authorization hold then begins releasing.

- Release time: Hold release takes 7 to 30 days depending on the network and the match between the pre-authorization amount and the settled amount. If the final folio matches the pre-authorization exactly, releases can happen within 24 to 72 hours. If the final folio differs significantly (the guest spent less on incidentals than was held, or the stay was extended at a different rate), the release can take the full 30 days.

- Why holds aren't charges: A hold reduces available credit but doesn't post a charge. The cardholder isn't paying interest on the held amount, isn't responsible for it long-term, and won't see it on their statement as a posted transaction. Holds only convert to charges through settlement.

Common failure points and how to prevent them

Four failure modes account for most corporate hotel CC authorization problems. Each has a specific fix.

- CCA form not attached to reservation: The finance team sends the form, the hotel acknowledges receipt, but the form doesn't get filed to the reservation in the property management system. At check-in the property treats the booking as card-not-present without authorization. Fix: confirm the form is filed by name to the reservation 48 hours before arrival.

- AVS mismatch on the form: The billing address on the CCA form doesn't match the corporate card's registered address. Fix: confirm the billing address matches before sending the form.

- Incidental hold exceeds card limit: The pre-authorization at check-in plus existing holds on the card from other bookings pushes total available credit below zero. The hold itself fails. Fix: confirm the card's available credit (not just total credit limit) is sufficient for the full stay plus incidentals.

- Post-stay charges added without authorization: The hotel adds charges (damage claims, late checkout, minibar disputes) after the guest has departed, using the card still on file. These are unauthorized under FCBA when they exceed the scope of the original CCA form, and they should be disputed.

The structural fix that closes all four failure modes is the virtual card. A virtual card generated per booking, capped at the exact authorized amount, with a merchant lock to the specific property, can only be charged for what the booking explicitly authorized. ITILITE issues per-trip virtual cards and reconfirms payment details with the hotel before arrival, so the authorization form is not in the chain at all.

FAQ

How long does hotel credit card authorization take?

The authorization request itself completes in 1 to 3 seconds, with a total visible delay of 5 to 15 seconds at check-in including verification checks and registration. Pre-authorization holds after checkout take 7 to 30 days to release, longer than any other merchant category, because the final folio amount often differs from the pre-authorization.

What is a pre-authorization hold on a hotel card?

A pre-authorization hold is a temporary reservation on the cardholder's available credit equal to the room rate plus the property's incidental amount (typically $50 to $200 per night). The hold doesn't post as a charge. Funds are reserved against the eventual settlement at checkout.

How long does it take for a hotel to release a pre-authorization hold?

Hold release takes 7 to 30 days depending on the card network and how closely the final folio matches the pre-authorization. Exact matches can release in 24 to 72 hours; significant differences can take the full 30 days. The hold itself isn't a charge; the cardholder doesn't pay interest on it.

Why did my hotel credit card authorization fail at check-in?

The most common causes are: the CCA form wasn't filed to the reservation, AVS mismatch between the form's billing address and the card's registered address, the pre-authorization amount exceeded available credit, or a fraud flag on a card-not-present transaction from an unusual location. Each has a different fix.

Can a hotel charge my credit card after checkout?

Hotels can attempt charges for incidentals or damages discovered after checkout if the card is still on file. These charges should match the scope authorized on the CCA form or by the guest at check-in. Charges beyond that scope are unauthorized under the Fair Credit Billing Act and can be disputed (https://www.law.cornell.edu/uscode/text/15/1643).

What is the difference between hotel credit card authorization and settlement?

Authorization is the hold placed on the card at check-in (and any incremental holds during the stay). Settlement is the final charge submitted at checkout that actually moves money from the cardholder's account to the hotel's account. Holds and settlement are separate transactions, which is why pending hold amounts often persist after the settled charge has already posted.

Ardra is a Content Strategy Manager at ITILITE with 6+ years of experience in travel and SaaS content. She holds a Master’s degree in Political Science from Lady Shri Ram College for Women and transitioned from academic research and travel content into SaaS content strategy.

She previously worked with JustWravel, where she focused on travel storytelling and digital content. Today, she specializes in SEO and AEO-driven content strategies that help businesses simplify complex travel and expense workflows into search-optimized narratives.

When she’s not working, Ardra is usually reading or watching films.

Eliminate Hotel CCA Forms & Payment Delays

A fully integrated corporate travel management software that dramatically reduces spends while improving user experience

.jpeg)

%20(1).png)

%20(1).png)

.jpeg)

.jpeg)

.jpeg)

.webp)

.jpeg)

.jpeg)

.webp)

.png)